Backtests create confidence.

Markets remove it.

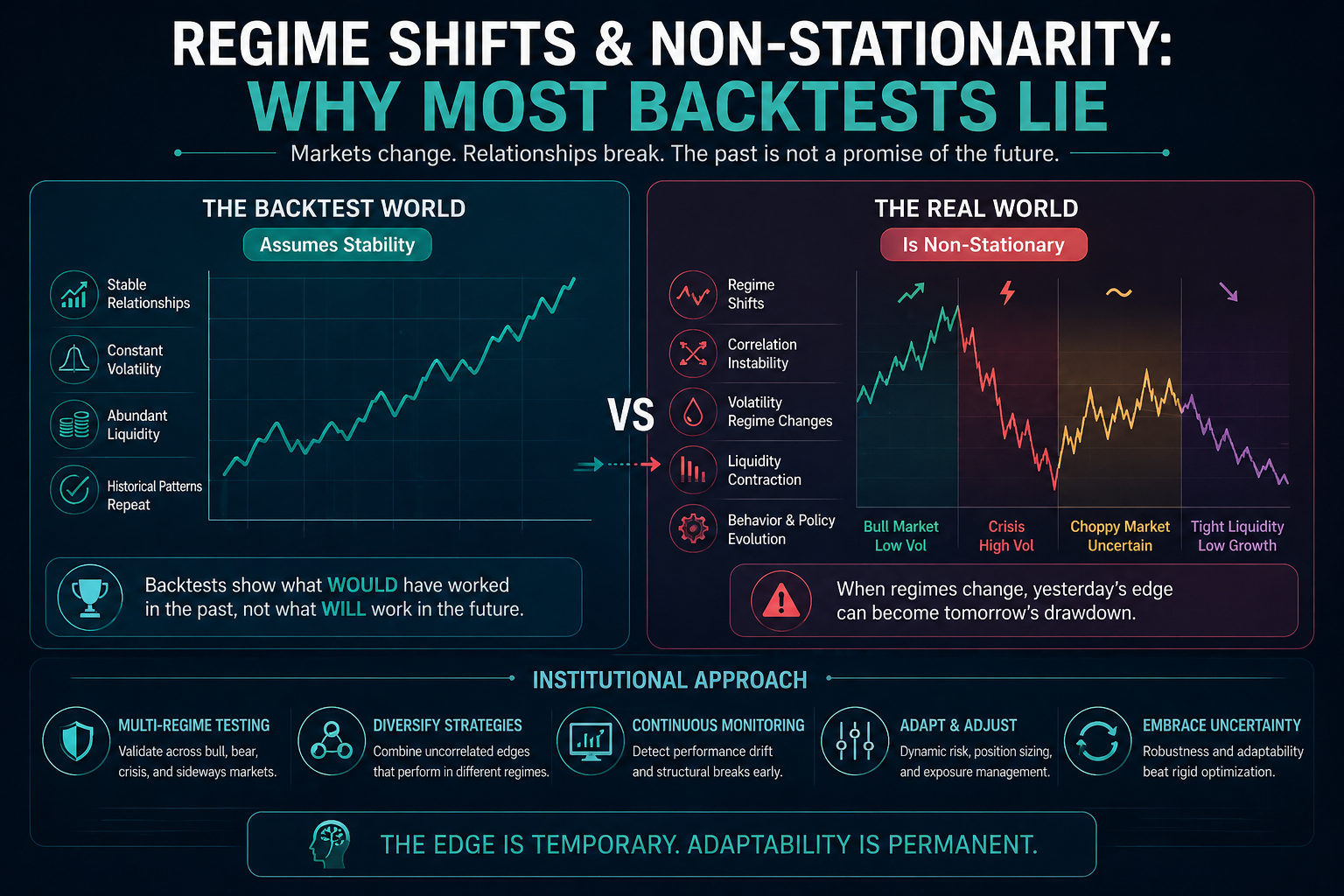

One of the most misunderstood realities in quantitative trading is that financial markets are non-stationary — meaning their statistical properties change over time.

At Linitics, we treat non-stationarity not as a risk — but as the defining condition of markets.

Understanding this is essential to building strategies that survive.

1. What Is Non-Stationarity?

In a stationary system:

- Mean returns are stable

- Volatility is predictable

- Relationships persist

Financial markets are not stationary.

They evolve.

Key properties that change over time:

- Volatility regimes

- Correlation structures

- Liquidity conditions

- Market participant behavior

- Macroeconomic drivers

A model trained on past data assumes stability.

Markets do not provide it.

2. The Problem with Backtests

Backtests implicitly assume:

- Historical relationships will persist

- Market structure remains constant

- Costs remain stable

- Liquidity is unchanged

These assumptions are rarely valid.

A strong backtest often reflects:

- A specific regime

- A favorable volatility environment

- A temporary inefficiency

When the regime changes, the edge disappears.

3. What Is a Regime Shift?

A regime shift is a structural change in market behavior.

Examples include:

- Low inflation → high inflation environments

- Zero interest rate → tightening cycles

- Low volatility → volatility expansion

- Liquidity abundance → liquidity contraction

These shifts alter:

- Strategy performance

- Risk characteristics

- Correlation patterns

A strategy built in one regime may fail in another.

4. Historical Examples of Regime Shifts

2000–2002 (Dot-Com Collapse)

- Momentum strategies reversed violently

- Growth collapsed

- Volatility spiked

2008 (Global Financial Crisis)

- Correlations converged toward 1

- Liquidity evaporated

- Many strategies failed simultaneously

2020 (COVID Shock)

- Extreme volatility expansion

- Rapid regime transitions

- Unprecedented policy response

2022 (Rate Regime Shift)

- Growth → value rotation

- Bond-equity correlation breakdown

- Factor instability

Each period invalidated previously successful models.

5. Why Backtests “Lie”

Backtests do not lie intentionally.

They mislead structurally.

Because they:

- Fit models to specific historical conditions

- Capture regime-dependent patterns

- Ignore future structural change

A backtest answers:

“What would have worked?”

It does not answer:

“What will continue to work?”

6. Overfitting vs Regime Dependency

Not all failure is overfitting.

A model can be:

- Statistically sound

- Economically logical

- Properly validated

And still fail.

Because:

The regime changed.

This distinction is critical:

- Overfitting = model error

- Regime shift = market evolution

Both produce failure.

But require different responses.

7. Correlation Instability

One of the most dangerous aspects of non-stationarity is:

Correlation is not stable

Examples:

- Stocks and bonds switching from negative to positive correlation

- Diversified portfolios becoming highly correlated in crises

Diversification assumptions often break during stress.

This creates hidden tail risk.

8. Volatility Regimes Change Behavior

Strategies behave differently under:

- Low volatility (range-bound markets)

- High volatility (trend or breakdown markets)

Examples:

- Mean reversion works better in low volatility

- Trend-following works better in high volatility

A strategy optimized in one regime will underperform in another.

9. Liquidity Regime Matters

Liquidity is not constant.

It changes based on:

- Market stress

- Policy conditions

- Institutional participation

During liquidity contraction:

- Spreads widen

- Slippage increases

- Execution fails

Backtests rarely capture liquidity stress accurately.

10. Institutional Approach to Non-Stationarity

Professional quant firms adapt through:

A. Multi-Regime Testing

Testing across different historical environments.

B. Strategy Diversification

Combining strategies that perform in different regimes.

C. Volatility Scaling

Adjusting exposure based on market conditions.

D. Continuous Monitoring

Detecting performance drift early.

E. Adaptive Systems

Incorporating dynamic risk and allocation frameworks.

The goal is not prediction.

It is adaptation.

11. Why Static Models Fail

A static model assumes:

- Fixed parameters

- Stable relationships

- Persistent edge

In a non-stationary market:

- Parameters drift

- Relationships break

- Edge decays

Static systems fail because markets evolve faster than models.

12. What This Means for Practitioners

Key implications:

- Backtests should be treated as conditional, not predictive

- Robustness matters more than peak performance

- Strategies must be monitored continuously

- Adaptation must be built into the system

The objective is not to eliminate uncertainty.

It is to survive it.

Final Thoughts

Markets are not stable systems.

They are adaptive ecosystems.

Non-stationarity ensures that:

- No strategy works forever

- No model remains optimal

- No backtest guarantees future performance

At Linitics, we design strategies with this constraint in mind — prioritizing adaptability, robustness, and continuous validation.

Because in quantitative trading:

The biggest risk is not being wrong.

It is assuming the future will look like the past.