Returns attract attention.

Drawdowns determine survival.

In quantitative trading, performance is not defined by peak returns — but by the ability to endure adverse sequences without irreversible capital impairment.

At Linitics, we treat drawdown control, leverage discipline, and convexity awareness as the core pillars of systematic survival.

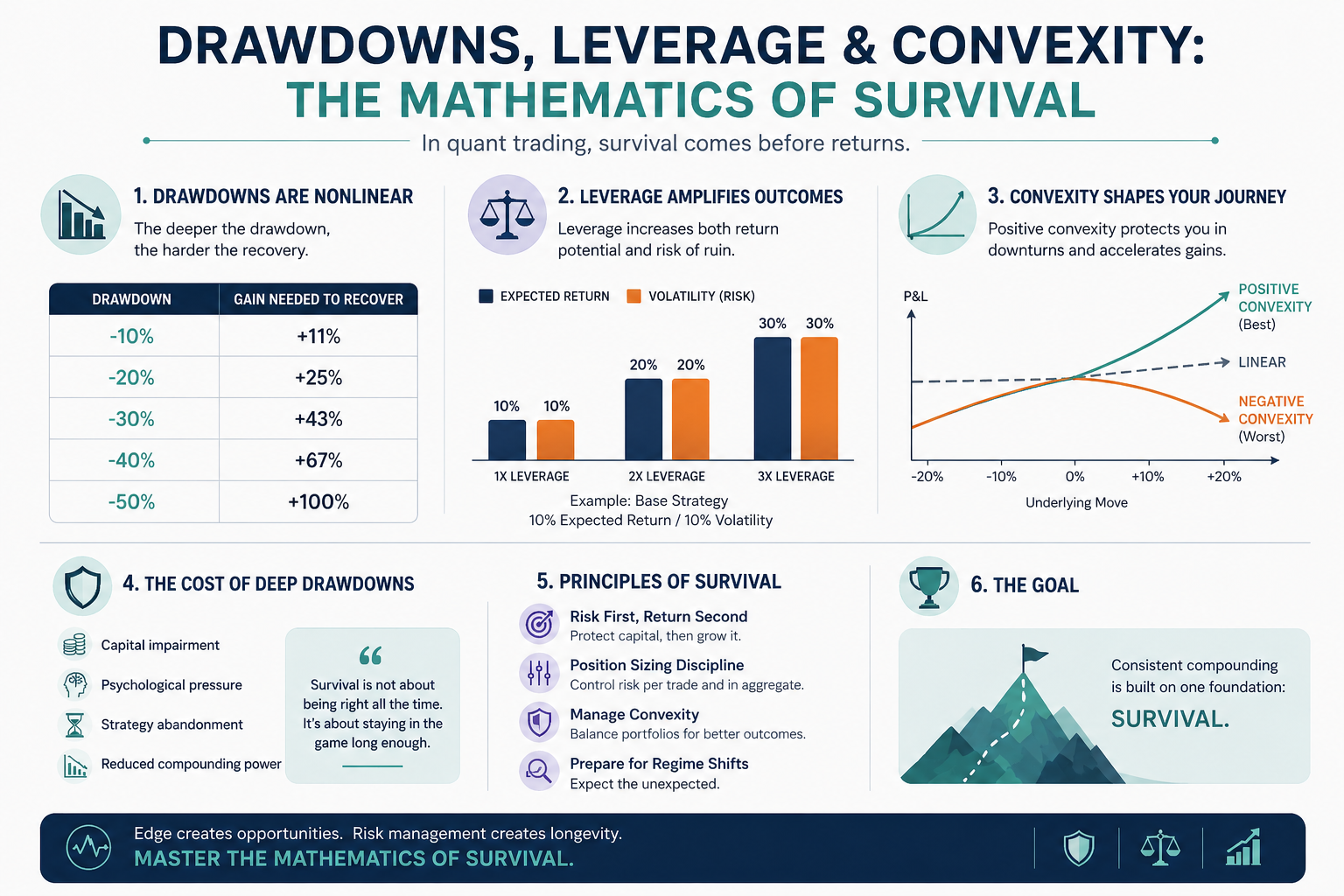

1. Drawdowns Are Not Linear Problems

A drawdown is not just a percentage loss.

It is a nonlinear recovery problem.

- A 10% loss requires ~11% gain to recover

- A 30% loss requires ~43% gain

- A 50% loss requires 100% gain

As drawdowns deepen, recovery becomes exponentially harder.

This creates a structural asymmetry:

Losses compound faster than gains recover.

2. The Hidden Cost of Deep Drawdowns

Beyond mathematics, drawdowns introduce:

- Capital impairment

- Reduced compounding base

- Psychological stress

- Strategy abandonment risk

Even a statistically sound strategy can fail if:

- Drawdowns exceed tolerance

- Capital is withdrawn

- Execution discipline breaks

Survival is not purely mathematical.

It is behavioral.

3. Leverage: Amplifier of Both Edge and Error

Leverage increases:

- Return potential

- Drawdown magnitude

- Sensitivity to volatility

- Risk of ruin

A strategy with:

- 10% expected return

- 10% volatility

Becomes, under 3× leverage:

- 30% expected return

- 30% volatility

But drawdowns scale as well — often faster due to volatility clustering.

Leverage does not create edge.

It magnifies outcomes.

4. Volatility Clustering & Leverage Risk

Markets exhibit volatility clustering:

- Calm periods → sudden expansion

- Low risk → abrupt high risk

Leverage applied during low volatility often leads to:

- Overexposure

- Sudden drawdown spikes

- Forced deleveraging

This is a common failure mode:

Leverage increases when risk appears low — precisely before it rises.

5. Convexity: The Shape of Risk

Convexity describes how returns respond to changes in underlying conditions.

Positive Convexity:

- Gains accelerate during favorable moves

- Losses are limited during adverse moves

Negative Convexity:

- Small consistent gains

- Occasional large losses

Many strategies (especially short volatility or premium-selling) exhibit negative convexity:

- Frequent small profits

- Rare but severe drawdowns

This creates misleading performance:

High win rate ≠ low risk.

6. The Trap of Smooth Equity Curves

Strategies with:

- High win rates

- Low volatility

- Smooth equity curves

Often hide:

- Tail risk

- Negative convexity

- Fragile assumptions

These strategies appear stable — until they fail suddenly.

The absence of volatility is not safety.

It is often delayed risk.

7. Risk of Ruin

Risk of ruin is the probability of losing enough capital to:

- Prevent recovery

- Force strategy shutdown

It depends on:

- Win rate

- Payoff ratio

- Position sizing

- Drawdown tolerance

Even profitable strategies can have high risk of ruin if:

- Position sizing is aggressive

- Drawdowns are large

- Losses cluster

Survival requires controlling tail risk — not just average outcomes.

8. Position Sizing as a Survival Tool

Position sizing determines:

- Drawdown depth

- Volatility of returns

- Longevity of strategy

Common frameworks:

- Fixed fractional risk

- Volatility scaling

- Kelly fraction (often reduced for safety)

Over-sizing is the fastest path to failure.

Under-sizing preserves optionality.

9. Convexity Engineering

Institutional portfolios manage convexity intentionally:

- Combine strategies with different payoff profiles

- Include tail-risk hedges

- Balance negative convexity with positive convexity

Examples:

- Trend-following (positive convexity)

- Options hedging structures

- Dynamic exposure reduction

The goal is not eliminating drawdowns.

It is controlling their shape.

10. The Role of Diversification

Diversification is not just about:

- Different assets

It is about:

- Different behaviors under stress

- Different convexity profiles

- Different regime responses

True diversification reduces:

- Tail risk

- Drawdown clustering

- Correlation spikes

But only if correlations are not assumed static.

11. Psychological Limits Define Practical Limits

Mathematical drawdown tolerance is not enough.

If a strategy has:

- 40% expected drawdown

But the operator can tolerate only:

- 15%

The strategy is not viable.

Practical survivability depends on:

- Behavioral discipline

- Capital structure

- Investor expectations

The best strategy is one that can be executed consistently.

12. The Institutional Perspective

Professional firms focus on:

- Drawdown control over return maximization

- Dynamic leverage adjustment

- Convexity balancing

- Stress testing across extreme scenarios

Because:

Survival is the prerequisite for compounding.

Final Thoughts

In quantitative trading:

- Returns determine attractiveness

- Risk determines sustainability

Drawdowns, leverage, and convexity define whether a strategy:

- Compounds capital

or - Terminates prematurely

At Linitics, we design strategies with survival as the primary constraint — ensuring that capital endures long enough for edge to compound.

Because in markets:

You do not fail because you were wrong.

You fail because you could not survive being wrong.