The distinction between proprietary trading firms and hedge funds is often misunderstood.

Both:

- Trade systematically

- Deploy capital in markets

- Use quantitative strategies

Yet structurally, they operate under fundamentally different constraints and incentives.

At Linitics, we view this distinction as critical—because structure determines:

- Risk behavior

- Strategy selection

- Performance consistency

- Scalability

This is not a difference in trading skill.

It is a difference in institutional design.

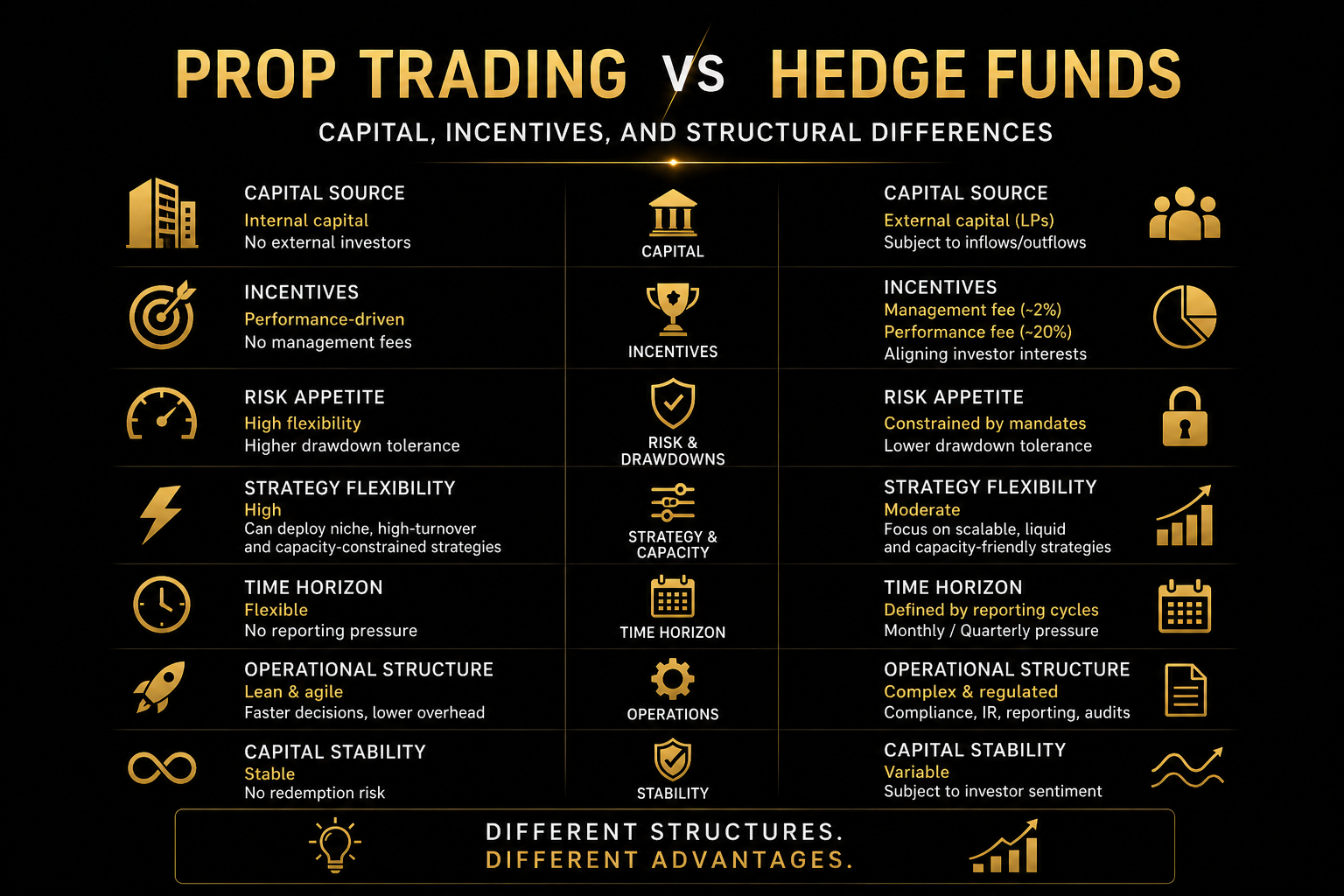

1. Capital Source: Internal vs External

Prop Trading Firms

- Trade internal capital

- No external investors

- No redemption pressure

Hedge Funds

- Manage external capital (LPs)

- Subject to inflows/outflows

- Investor expectations influence behavior

Implication:

Internal capital allows flexibility.

External capital introduces constraints.

2. Incentive Structures

Prop Firms

- Profit participation directly tied to performance

- No management fees

- Compensation is performance-driven

Hedge Funds

- Typically “2 and 20” structure:

- ~2% management fee

- ~20% performance fee

This creates:

- Asset gathering incentives

- Stability bias

- Risk-adjusted positioning

Implication:

Prop firms optimize for absolute performance.

Hedge funds optimize for risk-adjusted, investor-acceptable returns.

3. Risk Appetite & Drawdown Tolerance

Prop Firms

- Can tolerate higher volatility

- More flexible drawdown thresholds

- Faster risk reallocation

Hedge Funds

- Constrained by:

- Investor mandates

- Risk committees

- Redemption risk

Drawdowns lead to:

- Capital outflows

- Strategy pressure

- Potential shutdown

Implication:

Hedge funds must manage perception of risk—not just risk itself.

4. Strategy Selection & Deployment

Prop Firms

- Can deploy:

- Short-term strategies

- High-turnover systems

- Capacity-constrained alpha

Hedge Funds

- Prefer:

- Scalable strategies

- Institutional capacity

- Lower turnover

Because:

- Larger AUM requires liquidity

- Execution constraints increase

Implication:

Some strategies exist only in prop environments.

5. Time Horizon

Prop Firms

- Flexible time horizons

- Can pivot quickly

- No reporting pressure

Hedge Funds

- Structured reporting cycles:

- Monthly

- Quarterly

This creates:

- Short-term performance pressure

- Behavioral constraints

Implication:

Time horizon is often dictated by capital structure—not strategy logic.

6. Liquidity & Capacity Constraints

Prop Firms

- Smaller capital base

- Can operate in niche opportunities

- Lower market impact

Hedge Funds

- Large AUM

- Require deep liquidity

- Limited access to small inefficiencies

Implication:

Scale reduces opportunity set.

7. Operational Complexity

Prop Firms

- Lean structure

- Faster decision-making

- Lower administrative overhead

Hedge Funds

- Complex operations:

- Compliance

- Reporting

- Auditing

- Investor relations

This introduces:

- Slower adaptation

- Higher cost structures

8. Capital Stability

Prop Firms

- Stable capital base

- No redemption risk

Hedge Funds

- Capital is conditional

- Subject to:

- Performance cycles

- Investor sentiment

This creates:

- Forced de-risking

- Strategy distortion

Implication:

Stability of capital directly affects strategy stability.

9. Governance & Oversight

Hedge Funds

- Formal governance:

- Risk committees

- Compliance frameworks

- External oversight

Prop Firms

- Internal governance

- More autonomy

- Faster execution decisions

Implication:

Governance improves control—but reduces flexibility.

10. Performance vs Asset Growth

Prop Firms

- Focus on:

- Return on capital

- Efficiency

Hedge Funds

- Balance between:

- Performance

- Asset growth

Large AUM leads to:

- Strategy dilution

- Lower marginal returns

11. Scalability Trade-Off

Prop firms face:

- Limited scalability

- Capacity constraints

Hedge funds achieve:

- Capital scale

- Institutional reach

But often at the cost of:

- Reduced agility

- Lower alpha per unit capital

12. Where the Real Edge Lies

The industry often debates:

- Which model performs better

The reality:

They optimize for different objectives.

| Dimension | Prop Trading | Hedge Funds |

|---|---|---|

| Capital | Internal | External |

| Incentives | Performance-driven | Fee + performance |

| Flexibility | High | Moderate |

| Scale | Limited | High |

| Stability | High (capital) | Variable |

| Constraints | Low | High |

13. Convergence Trends

The line between the two is evolving:

- Prop firms are institutionalizing

- Hedge funds are adopting systematic strategies

- Technology is bridging gaps

However:

The structural differences remain intact.

14. The Linitics Perspective

At Linitics, we recognize:

- The flexibility of prop trading

- The discipline of institutional frameworks

Our approach integrates:

- Systematic strategy design

- Institutional-grade risk management

- Capital efficiency

- Scalable infrastructure

Because:

The future of trading is not one model replacing another.

It is:

Combining the strengths of both.

Final Thoughts

Prop trading firms and hedge funds operate in the same markets—

But under different structural realities.

Understanding these differences is essential for:

- Strategy design

- Capital allocation

- Risk management

- Business building

Because in trading:

- Strategy matters

- Execution matters

But structure determines:

Whether any of it scales.

At Linitics, we build systems designed not just to trade—

But to operate within the realities of modern capital markets.