Most quant strategies fail not because they are wrong.

They fail because they are too large.

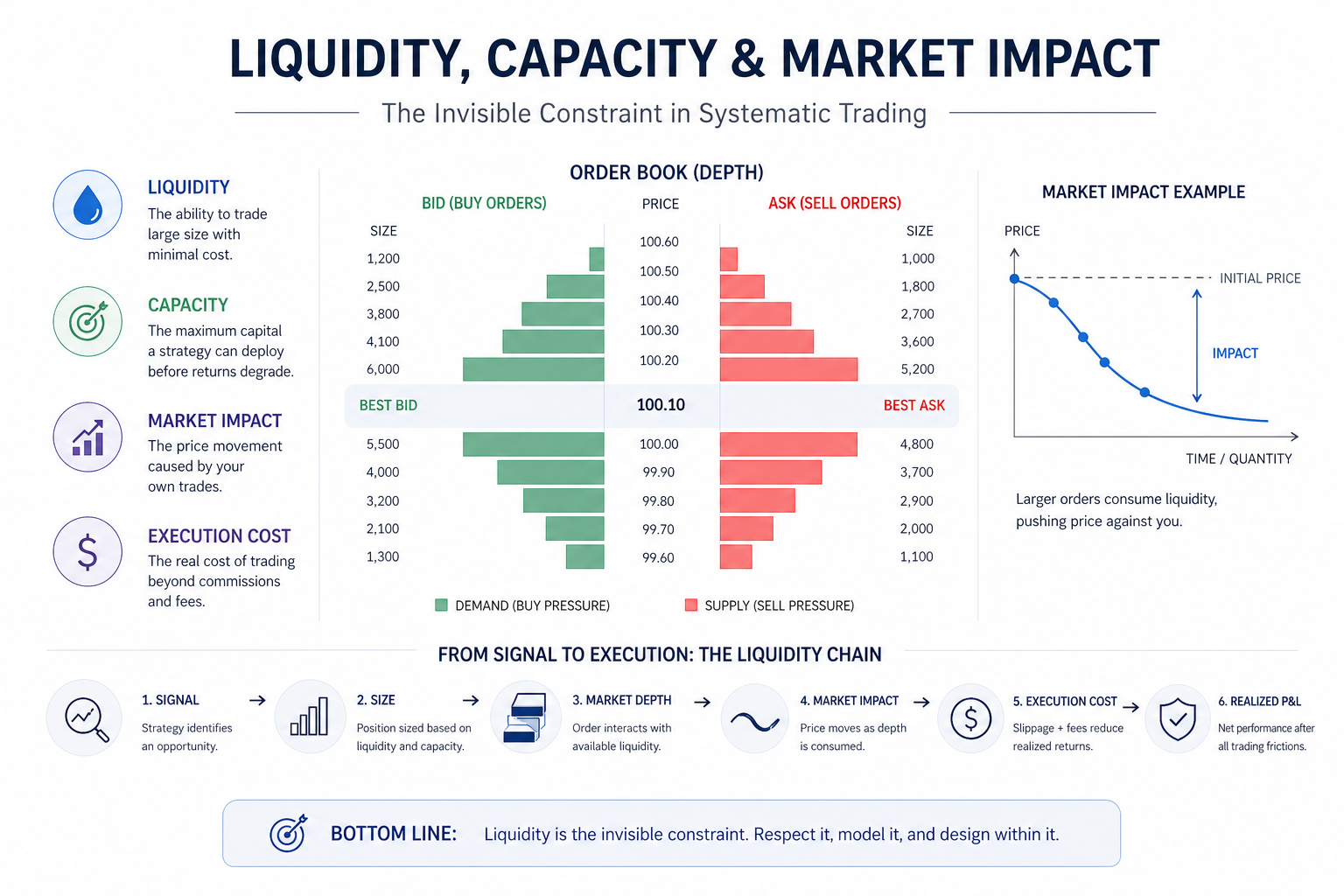

In systematic trading, the real constraint is not signal quality — it is liquidity.

At Linitics, we treat liquidity, capacity, and market impact as first-order design variables, not afterthoughts.

Because capital does not operate in isolation.

It interacts with the market.

1. Liquidity: The Foundation of Execution

Liquidity determines:

- How easily positions can be entered

- How efficiently positions can be exited

- How much slippage is incurred

It is shaped by:

- Trading volume

- Order book depth

- Bid–ask spread

- Market participation

A strategy without liquidity awareness is not deployable.

It is theoretical.

2. The Illusion of Frictionless Markets

Backtests assume:

- Instant fills

- Infinite liquidity

- Fixed spreads

- No impact

Reality introduces friction:

- Orders move price

- Execution occurs across levels

- Liquidity vanishes under stress

The larger the capital, the larger the deviation from backtest assumptions.

3. Market Impact: The Cost You Create

Market impact is the price movement caused by your own trades.

There are two components:

A. Temporary Impact

- Price moves during execution

- Partially reverts after completion

B. Permanent Impact

- Reflects information conveyed to market

- Alters price structure

As size increases:

- Impact grows nonlinearly

- Execution efficiency deteriorates

At scale, you become part of the market.

4. Capacity: The Hard Limit of Alpha

Every strategy has a capacity ceiling.

Capacity is determined by:

- Liquidity of instruments

- Trade frequency

- Holding period

- Turnover

- Market depth

Beyond capacity:

- Returns decline

- Risk increases

- Execution fails

Capacity is not estimated by backtest.

It is constrained by market structure.

5. Participation Rate: A Key Institutional Metric

Professional traders monitor:

Participation Rate = Order Size / Market Volume

Typical institutional constraints:

- ≤ 5%–10% of average volume

Higher participation leads to:

- Increased impact

- Detection by other participants

- Adverse price movement

The market adapts to visible flow.

6. Slippage: The Silent Performance Killer

Slippage is:

The difference between expected price and executed price

At scale:

- Entry slippage increases

- Exit slippage increases

- Stop execution worsens

Even small slippage changes can:

- Destroy Sharpe ratio

- Increase drawdowns

- Eliminate edge

Most retail backtests underestimate slippage significantly.

7. Turnover vs Capacity Trade-Off

High-turnover strategies:

- Generate frequent signals

- Face higher cost drag

- Have lower capacity

Low-turnover strategies:

- Scale more efficiently

- Have lower execution costs

- Offer higher capacity

There is a structural trade-off:

Higher frequency → Lower scalability

8. Liquidity During Stress

Liquidity is not constant.

During stress:

- Bid–ask spreads widen

- Order book depth disappears

- Slippage spikes

- Execution delays increase

Strategies that appear stable in normal conditions may fail under:

- Volatility spikes

- Market dislocations

- Forced liquidation environments

Stress exposes true capacity.

9. Crowding & Flow Detection

As strategies scale:

- Order patterns become detectable

- Other participants anticipate flows

- Execution becomes adversarial

This leads to:

- Front-running

- Adverse selection

- Alpha decay

The more visible the flow, the weaker the edge.

10. Execution as a Source of Edge

At institutional scale, execution is not operational.

It is strategic.

Key elements include:

- Order slicing algorithms

- Smart routing

- Timing optimization

- Liquidity sourcing

Execution quality can determine whether:

- A strategy remains profitable

or - Alpha is fully consumed by costs

11. Designing Liquidity-Aware Strategies

Institutional frameworks incorporate:

A. Liquidity Filters

Trade only instruments with sufficient depth.

B. Capacity Modeling

Estimate capital limits before deployment.

C. Turnover Control

Reduce unnecessary trading.

D. Impact Modeling

Simulate execution cost realistically.

E. Dynamic Position Sizing

Adjust size based on liquidity conditions.

Strategies are designed for deployment — not just discovery.

12. Implications for Smaller Traders

Smaller capital has advantages:

- Lower market impact

- Faster execution

- Access to niche inefficiencies

Scaling is not always desirable.

In many cases:

Smaller capital = higher efficiency

Understanding when not to scale is as important as knowing how to scale.

Final Thoughts

Liquidity, capacity, and market impact define the real boundaries of systematic trading.

They are invisible in backtests.

But unavoidable in reality.

At Linitics, we treat these constraints as core components of strategy design — ensuring that models remain viable under real capital conditions.

Because in quantitative trading:

Edge may generate returns.

But liquidity determines whether those returns can be realized.