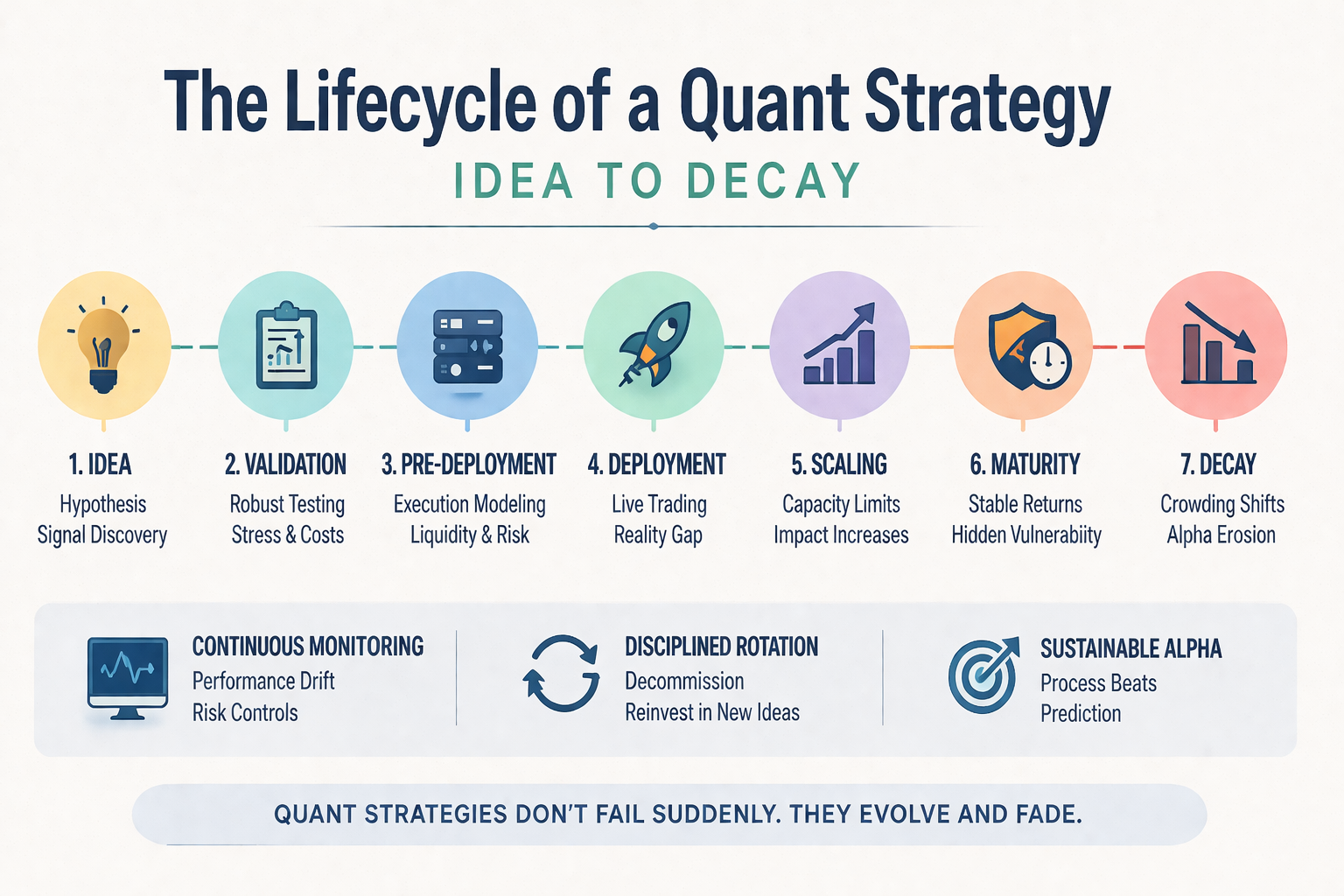

Quantitative strategies do not fail suddenly.

They evolve — and eventually decay.

Understanding this lifecycle is essential for anyone attempting to build systematic trading systems that survive beyond short-term success.

At Linitics, strategies are treated not as static models, but as dynamic capital assets that move through identifiable stages—each with distinct risks, constraints, and failure modes.

1. Idea: Signal Discovery vs Signal Illusion

Every strategy begins with a hypothesis.

Examples include:

- Momentum persistence

- Mean reversion

- Volatility expansion

- Cross-asset relationships

- Behavioral inefficiencies

However, most “ideas” originate from:

- Data mining

- Parameter exploration

- Accidental correlations

The key distinction:

Signal vs coincidence

Institutional-grade idea generation requires:

- Economic rationale

- Behavioral or structural explanation

- Cross-market plausibility

Without this, the strategy is not an idea — it is a statistical accident.

2. Validation: Destroying False Confidence

Validation is not about proving a model works.

It is about attempting to prove it does not.

Core validation principles:

- Out-of-sample testing

- Parameter robustness (not precision)

- Cross-asset validation

- Regime diversity testing

- Transaction cost integration

A critical insight:

If performance survives aggressive degradation assumptions, it is likely real.

If it collapses under minor perturbation, it was never robust.

Most strategies fail here — but many are mistakenly promoted forward.

3. Pre-Deployment: The Reality Filter

Before live capital, a professional process introduces friction:

- Slippage assumptions

- Latency considerations

- Liquidity constraints

- Execution modeling

- Capital scaling tests

This stage answers:

“Does this survive the real world?”

Many strategies that pass validation fail at this stage because:

- Costs were underestimated

- Liquidity was assumed infinite

- Turnover was unrealistic

The difference between a model and a business emerges here.

4. Deployment: The Reality Gap

Live trading introduces what is often called the reality gap:

Backtest performance ≠ Live performance

Common causes:

- Microstructure noise

- Spread variation

- Partial fills

- Execution delay

- Regime mismatch at launch

Institutional deployment is gradual:

- Reduced capital allocation

- Monitoring windows

- Performance benchmarking vs expectation

Deployment is not confirmation.

It is probation.

5. Scaling: Where Most Strategies Break

Scaling introduces nonlinear effects:

- Market impact increases

- Slippage widens

- Alpha compresses

- Execution quality deteriorates

A strategy that performs at small scale may fail at institutional size.

Key constraints:

- Liquidity

- Capacity

- Turnover

- Correlation with market structure

Scaling is not growth.

It is stress.

6. Maturity: Stable but Vulnerable

At maturity, the strategy:

- Produces consistent returns

- Has known risk characteristics

- Is integrated into capital allocation

This is the most deceptive phase.

Because:

- Confidence is highest

- Risk appears controlled

- Capital allocation increases

Yet beneath stability:

- Crowding may be building

- Edge may be compressing

- Regime dependency may be forming

Mature strategies fail when treated as permanent.

7. Decay: The Inevitable Phase

All quant strategies decay.

Drivers include:

A. Crowding

Capital flows into successful signals.

B. Structural Market Change

Regulation, technology, liquidity evolution.

C. Regime Shifts

Interest rates, volatility cycles, macro transitions.

D. Information Diffusion

Edge becomes widely known.

Empirical research shows even well-known factors experience multi-year underperformance cycles.

Decay is not a failure.

It is a certainty.

8. Detection of Decay

Institutional monitoring focuses on:

- Rolling Sharpe degradation

- Increasing drawdown frequency

- Correlation instability

- Execution cost drift

- Volatility mismatch

The challenge is not detecting collapse.

It is detecting early deterioration.

Early detection allows controlled de-risking.

9. Decommissioning: A Professional Discipline

Retail traders hold on too long.

Institutional firms define exit rules:

- Performance below threshold

- Risk-adjusted deterioration

- Structural break detection

A strategy is retired not when it loses money —

but when it loses statistical validity.

Capital is reallocated.

Emotion is removed.

10. The Portfolio of Strategies Approach

No serious quant operation depends on a single strategy.

Instead, they operate:

- Multiple strategies

- Across lifecycle stages

- With varying correlations

- With staggered decay timelines

This creates:

- Stability

- Diversification

- Continuous alpha pipeline

The system survives even when individual strategies fail.

11. The Continuous Research Flywheel

Institutional survival depends on:

Idea → Validation → Deployment → Monitoring → Decay → Replacement

This loop never stops.

Research is not a phase.

It is infrastructure.

12. Where Most Practitioners Fail

Common mistakes:

- Treating backtest as truth

- Over-allocating early

- Ignoring costs

- Scaling too quickly

- Holding decaying strategies

- Lack of pipeline

The issue is not intelligence.

It is process absence.

Final Thoughts

A quant strategy is not an asset.

It is a temporary edge.

Understanding its lifecycle transforms trading from:

Model building → Capital engineering

At Linitics, strategies are:

- Continuously validated

- Carefully deployed

- Actively monitored

- Systematically replaced

Because long-term success in quant trading does not come from finding one great strategy.

It comes from managing many imperfect ones — over time.